Rationale

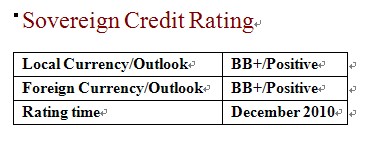

Dagong assigns “BB+” to

both the local and foreign currency long term sovereign credit ratings of the

Oriental Republic of Uruguay (hereinafter referred to as “Uruguay”) based on a comprehensive

analysis of its potential debt demand and realistic solvency risk etc..

With the improvement of

the fiscal deficit, the government debt has been substantially reduced in recent

years. As of the end of 2009, the central government outstanding debt to GDP

ratio had declined to 37.6% from 84.2% in 2003, but the non financial public

sector debt is still at a relatively high level of 59.7%. The recent

debt-managing programs helped to optimize its debt structure. The proportion of

5-year and more than 5-year debt has increased to 68.8% of total, reducing its

short-term debt pressure. However, the fact that the foreign currency debt

accounts for 73.0%, which is a high level, is one of the main negative factors

to its debt solvency. In addition,

the relative big size of contingent debt burden is another risk exposure of

Uruguay government. Considering that

the fiscal condition will be improved in the future, the debt scale would be

further reduced.

Overall, the improving

policy framework and low leverage level of the financial sector cut down the

shock brought by the international financial crisis. The improvement of the

fiscal condition and the decline of the debt rate enhance the government

solvency. However, the absence of driving force behind its long-term economic

growth and still high debt repaying pressure make its debt solvency risk at a

middle level. It can be specified as:

l

The reform after its financial crisis

in 2002 strengthened the compatibility of Uruguay’s

overall economic policy framework, producing a high growth rate. Its capability

against the Latin America shock, especial Argentina economic and financial

crisis, has been improved markedly. However, the high inflation and low size of

private investment restrict its long-term economic growing potential.

l

The strict fiscal discipline made the

fiscal deficit decrease. Though the international financial crisis and the

drought made the deficit increase in 2009, the size is still in a reasonable

scale. The improvement in fiscal condition will help the government realize its

aim of reducing the debt to 40% of its GDP.

l

The abundant international reserve

and the declining external debt improve its external liquidity. Although there

was capital flight in the international crisis, it has been under control all

the time. The strengthening tendency of Uruguay peso is helpful to reduce its

debt repaying pressure.

Outlook

The

reforms in recent years improve the Uruguay capability against the

regional economic shocks. The lower degree of economic opening up, leverage in

the financial sector and the exposure to the toxic assets reduced the shock

extent of international economic crisis. However, its high inflation rate and

small size of private investment limit its economic growth potential in the

medium term. The improvement in fiscal situation in the future will be helpful

for the government to further reduce the debt size, but there is still a long

way before the government realizes its debt-reducing target. Relative low

domestic risks, high short-term growth anticipation and abundant foreign reserve

improve the external liquidity and the government financing ability. The stabilization of peso could also

reduce the debt repaying pressure of the government. As a result, Dagong keeps

the positive outlook for Uruguay government’s local and

foreign currency credit rating in the next 1-2 years